Fill Out a Valid Nevada Employment Security Division Template

Fill Out a Valid Nevada Employment Security Division Template

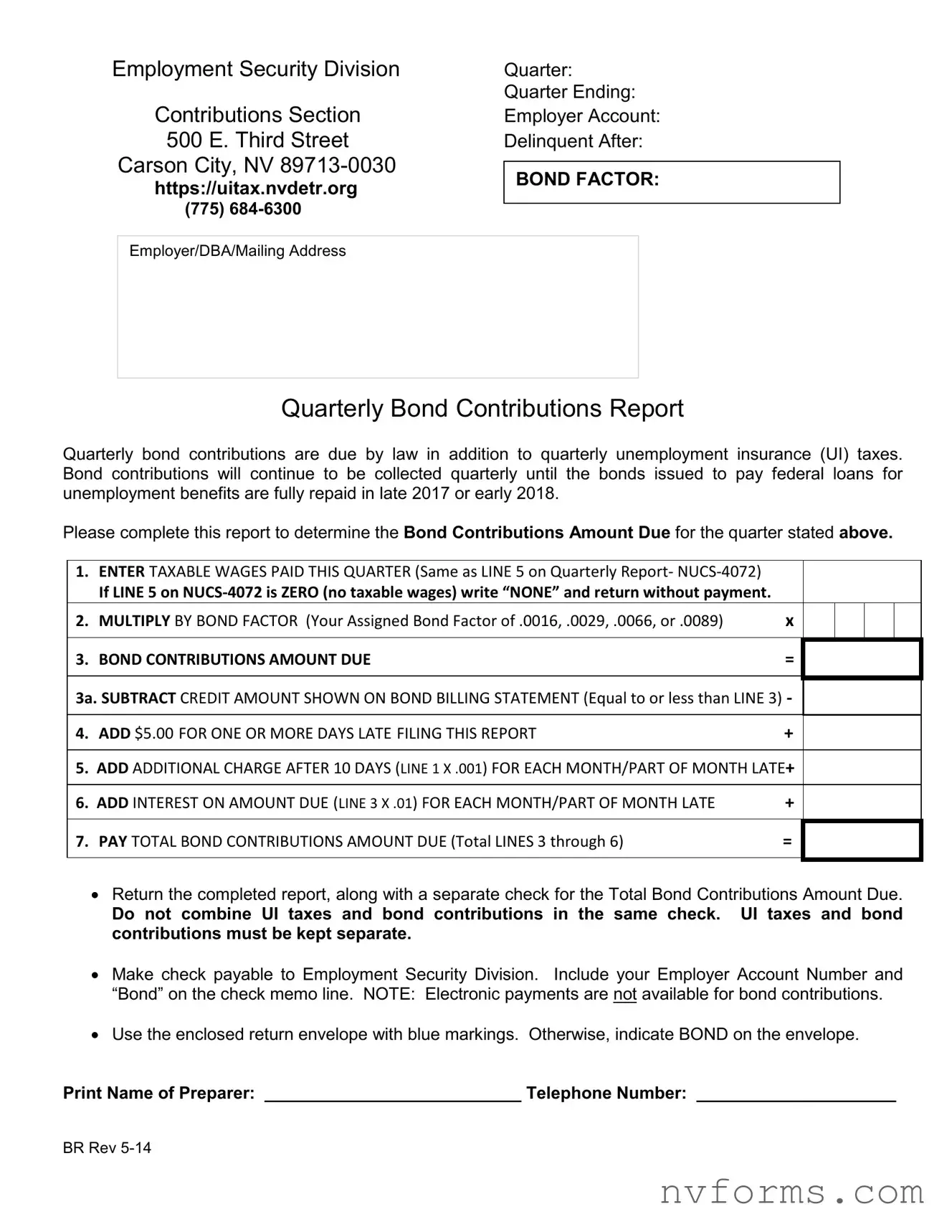

In Nevada, businesses are familiar with the responsibilities that come with employing individuals, one of which involves the Nevada Employment Security Division form. This form, utilized by the Employment Security Division's Contributions Section located at 500 E. Third Street in Carson City, plays a crucial role in maintaining the balance of the state's unemployment insurance (UI) system. Serving as a report for quarterly bond contributions in addition to the regular UI taxes, this form is vital for employers to complete accurately and on time. Businesses are required to calculate their bond contributions based on taxable wages paid within the quarter, employing a specific bond factor assigned to them, which could range from .0016 to .0089. The form details a step-by-step calculation for determining the amount due, including any adjustments for late filings or late payments, which incur additional charges and interest. Employers must then submit this amount separately from their UI taxes, using a check made payable to the Employment Security Division and marking it with their Employer Account Number and “Bond.” It’s important to note that this method of contribution will persist until the bonds issued for federal loans for unemployment benefits are completely repaid, anticipated by late 2017 or early 2018. Despite the digital era, electronic payments are not accepted for bond contributions, specifying a more traditional approach to fulfilling this obligation. This form, by facilitating the collection of quarterly bond contributions, ensures the stability and continuity of unemployment benefits within the state, highlighting the importance of compliance by all Nevada employers.

Employment Security Division

Contributions Section

500 E. Third Street

Carson City, NV

https://uitax.nvdetr.org

(775)

Quarter:

Quarter Ending:

Employer Account:

Delinquent After:

BOND FACTOR:

Employer/DBA/Mailing Address

Quarterly Bond Contributions Report

Quarterly bond contributions are due by law in addition to quarterly unemployment insurance (UI) taxes. Bond contributions will continue to be collected quarterly until the bonds issued to pay federal loans for unemployment benefits are fully repaid in late 2017 or early 2018.

Please complete this report to determine the Bond Contributions Amount Due for the quarter stated above.

1.ENTER TAXABLE WAGES PAID THIS QUARTER (Same as LINE 5 on Quarterly Report-

If LINE 5 on

2. |

MULTIPLY BY BOND FACTOR (Your Assigned Bond Factor of .0016, .0029, .0066, or .0089) |

x |

|

|

|

|

|

|

|

|

|

|

|

3. |

BOND CONTRIBUTIONS AMOUNT DUE |

= |

|

|

|

|

|

|

|

|

|

|

|

3a. SUBTRACT CREDIT AMOUNT SHOWN ON BOND BILLING STATEMENT (Equal to or less than LINE 3) -

4. ADD $5.00 FOR ONE OR MORE DAYS LATE FILING THIS REPORT |

+ |

5.ADD ADDITIONAL CHARGE AFTER 10 DAYS (LINE 1 X .001) FOR EACH MONTH/PART OF MONTH LATE+

6.ADD INTEREST ON AMOUNT DUE (LINE 3 X .01) FOR EACH MONTH/PART OF MONTH LATE

7.PAY TOTAL BOND CONTRIBUTIONS AMOUNT DUE (Total LINES 3 through 6)

+

= |

•Return the completed report, along with a separate check for the Total Bond Contributions Amount Due.

Do not combine UI taxes and bond contributions in the same check. UI taxes and bond contributions must be kept separate.

•Make check payable to Employment Security Division. Include your Employer Account Number and “Bond” on the check memo line. NOTE: Electronic payments are not available for bond contributions.

•Use the enclosed return envelope with blue markings. Otherwise, indicate BOND on the envelope.

Print Name of Preparer: ___________________________ Telephone Number: _____________________

BR Rev

| # | Fact |

|---|---|

| 1 | The form is issued by the Employment Security Division Contributions Section located at 500 E. Third Street, Carson City, NV 89713-0030. |

| 2 | The official website to obtain this form is https://uitax.nvdetr.org. |

| 3 | For inquiries, one can call (775) 684-6300. |

| 4 | Quarterly bond contributions are a mandatory addition to quarterly unemployment insurance (UI) taxes. |

| 5 | Bond contributions are collected to repay bonds issued for federal loans for unemployment benefits. |

| 6 | Full repayment of the bonds is anticipated by late 2017 or early 2018. |

| 7 | The form requires employers to calculate the Bond Contributions Amount Due using taxable wages and an assigned bond factor. |

| 8 | Late filing of this report incurs additional charges, compounded monthly. |

| 9 | Payments for bond contributions cannot be made electronically and must not be combined with UI taxes. |

| 10 | Users are instructed to make checks payable to Employment Security Division and to include their Employer Account Number as well as the word "Bond" on the check's memo line. |

Filing the Nevada Employment Security Division form is a key step for employers in Nevada to comply with state regulations regarding unemployment benefits. This form helps determine the quarterly bond contributions that are necessary in addition to the regular unemployment insurance (UI) taxes. These contributions are temporary and are aimed at repaying bonds issued to cover federal loans for unemployment benefits. They are to be collected until the bonds are fully repaid, expectedly by late 2017 or early 2018. It's important to complete this report accurately to avoid any delays or penalties associated with the bond contributions. Here are the steps to guide you through filling out the form:

It is crucial to follow these steps carefully and ensure that the report, along with the payment, is submitted on time. Failure to comply could result in penalties or interest charges, which could further complicate the financial responsibilities of your business towards unemployment insurance and bond contributions in Nevada.

What is the purpose of the Nevada Employment Security Division form?

The form is designed for employers to report and pay quarterly bond contributions which are required by law in addition to the regular quarterly unemployment insurance (UI) taxes. These contributions help repay the bonds issued to pay federal loans for unemployment benefits. They are collected until the bonds are fully repaid, expected to be in late 2017 or early 2018.

Where can this form be submitted?

The completed form should be sent to the Employment Security Division Contributions Section, located at 500 E. Third Street, Carson City, NV 89713-0030. Employers should use the enclosed return envelope with blue markings and indicate "BOND" on the envelope for clarity.

What is the deadline for filing this report?

Quarterly bond contributions must be submitted by the due date listed on the form under "Delinquent After" to avoid penalties. This date varies each quarter, and timely submission is important to prevent additional charges.

How is the Bond Contributions Amount Due calculated?

To determine the amount due, first, enter the taxable wages paid during the quarter. Then, multiply this number by your assigned bond factor (ranging from .0016 to .0089). If applicable, subtract any credit amount shown on your bond billing statement from this result. Late submissions require adding a late filing fee of $5.00 plus an additional charge and interest for each month or part of a month the payment is late.

What if my business had no taxable wages this quarter?

If there were no taxable wages for the quarter (Line 5 on NUCS-4072 is zero), write "NONE" on the form and return it without payment. This indicates to the Employment Security Division that your business did not engage in taxable activity for that quarter.

Can bond contributions be paid electronically?

No, electronic payments for bond contributions are not accepted. Payments must be made by check, which should be made payable to the Employment Security Division. Furthermore, it's important to include your Employer Account Number and denote "Bond" on the check's memo line to ensure proper processing.

Must bond contributions and UI taxes be paid together?

No, bond contributions and UI taxes should not be combined in the same payment. They must be paid separately to ensure accurate processing and allocation by the Employment Security Division.

How should checks for bond contributions be made out?

Checks should be made payable to the Employment Security Division. Be sure to include your Employer Account Number and the word "Bond" on the memo line of your check to clarify the purpose of the payment.

Who should I contact if I have questions about filling out the form or my bond contributions?

For questions or more information, you can visit https://uitax.nvdetr.org or call the Employment Security Division at (775) 684-6300. These resources can provide assistance with any inquiries regarding the form or bond contributions.

What should I do if I submit the bond contribution report late?

If the report is filed after the due date, a $5.00 fee is added for one or more days of late filing. Additional charges accumulate at a rate of .001 of Line 1 for each month, or part of a month, that the report and payment are late, along with an interest charge on the amount due (Line 3 x .01) for each month or part of a month late. Calculate your total due including these late fees and submit payment as soon as possible to minimize further penalties.

When completing the Nevada Employment Security Division form, individuals often encounter a few common pitfalls that can lead to errors in their submission. Understanding these mistakes ahead of time can help ensure that the process is smooth and free from avoidable errors. Here, we outline four frequent mistakes to watch for.

Incorrect Taxable Wages Entry: A common error is inaccurately entering the taxable wages paid during the quarter. This figure should match the amount reported on LINE 5 of the Quarterly Report- NUCS-4072. If no taxable wages were paid during the quarter, it's crucial to write “NONE” and return the form without payment. Misreporting this amount can lead to incorrect bond contribution calculations.

Misapplication of the Bond Factor: Another mistake is incorrectly applying the bond factor to the taxable wages. The form specifies using your assigned bond factor, which could be .0016, .0029, .0066, or .0089, to calculate the bond contributions amount due. An error in this step can significantly affect the total contributions due, potentially leading to underpayment or overpayment.

Failing to Adjust for Credits and Penalties: Failing to properly subtract the credit amount shown on the Bond Billing Statement or incorrectly adding late filing fees and interest for late payments complicates the process. The form requires subtracting the credit amount (if applicable) from the bond contributions amount due and adding specific charges for late filing and interest on late payments. Neglecting these adjustments can result in incorrect payment amounts being submitted.

Combining Payments for UI Taxes and Bond Contributions: A final frequent mistake is combining payments for UI taxes and bond contributions into a single check. The instructions clearly state that these payments must be kept separate and provide specific guidance on how each should be made out and submitted. This mistake can cause processing delays and potentially lead to penalties for not properly segregating the funds as required by the instructions.

By paying careful attention to these areas, individuals can minimize errors and ensure they are in compliance with the requirements set forth by the Nevada Employment Security Division. Always verify your entries and calculations, and remember to keep UI tax and bond contribution payments separate to avoid any issues with your submission.

When handling business matters related to the Nevada Employment Security Division, especially regarding the contributions section, it is vital to be aware of accompanying forms and documents that are often necessary for a complete and compliant submission process. These documents are crucial for various reasons, such as ensuring accurate reporting, compliance with state laws, and maintaining proper records for future reference. Here's a closer look at some of the commonly used documents alongside the Nevada Employment Security Division form.

Each of these documents plays a specific role in ensuring the smooth operation of employment and unemployment reporting and compliance within Nevada. Employers must familiarize themselves with these forms to avoid compliance issues and to streamline the process of reporting to the Nevada Employment Security Division. Keeping accurate records and promptly addressing any required submissions will help in maintaining good standing with state authorities and ensuring the well-being of both the business and its employees.

The Nevada Employment Security Division form is similar to other government forms designed to collect financial information from businesses, particularly those related to taxes and contributions. These similarities can be observed in structure, required information, and processing methods. For instance:

This form, like the Nevada Employment Security Division form, is used by employers to report taxable wages and calculate the amount of unemployment insurance tax due for the quarter. Both forms require employers to enter their business identification details, such as the Employer Account Number, and specify the quarter for which the report is being filed. They share a straightforward calculation process, where employers must input their total taxable wages, apply a specified rate (in the case of NUCS-4072, the unemployment insurance rate; for the bond contributions form, the bond factor rate), and then determine the amount due. Furthermore, both documents have provisions for adjustments based on prior contributions or credits and include late fees and interest for overdue payments. The emphasis on clear calculations and the importance of timely, accurate submissions underscores their role in maintaining compliance with state employment and taxation laws.

The Internal Revenue Service (IRS) Form 941 shares several key elements with the Nevada Employment Security Division form, despite covering federal taxation responsibilities. Employers use Form 941 to report income taxes, social security tax, or Medicare tax withheld from employees' paychecks and to pay the employer's portion of social security or Medicare tax. Similar to the Nevada form, Form 941 is structured to collect comprehensive employment and wage details for a specific quarter. Both forms necessitate meticulous record-keeping, as they require the calculation of taxes or contributions based on the wages paid to employees during the quarter. They include instructions for calculating the total amount owed, adjusting for any previous overpayments or credits, and adding penalties for late submissions. These forms underline the interconnectedness of federal and state tax and contribution systems, demonstrating how businesses must navigate multiple layers of compliance.

When it comes to filling out the Nevada Employment Security Division form, particularly for quarter bond contributions, attention to detail is critical. The form is designed to ensure that employers contribute accurately to the bond that's paying off federal loans for unemployment benefits. Here are some guidelines on what to do and what not to do while completing this form:

Do:

Don't:

Following these guidelines will help ensure that the process of reporting and contributing to the bond for unemployment benefits is as smooth and error-free as possible. It's all about maintaining accuracy, adhering to deadlines, and keeping payments separate for the Employment Security Division to process them efficiently.

Understanding the Nevada Employment Security Division form and its requirements for quarterly bond contributions can sometimes be confusing. Here are five common misconceptions about this document and the processes it details:

Clearing up these misconceptions can help employers better navigate their responsibilities regarding quarterly bond contributions and avoid unnecessary penalties. It's important for businesses to pay close attention to deadlines and requirements as set forth by the Nevada Employment Security Division to ensure compliance.

Understanding the process and requirements for filling out the Nevada Employment Security Division form for Quarterly Bond Contributions is crucial for employers. Here are four key takeaways that can help ensure compliance and accuracy:

By closely following these guidelines, employers can navigate the requirements for bond contributions efficiently, ensuring compliance with state regulations and supporting the Unemployment Insurance system's integrity.

Nevada Unemployment Maximum Weekly Benefit 2023 - Nevada's Employment Security Division uses information from the NUCS 4072 for unemployment insurance fund management.

Ca Dmv Reg 256 - Questions on the form address past driving infringements, including DUIs, to assess eligibility for certification.

Does an Accident Go on Your Record If No Police Report Is Filed - Designed for Nevada traffic incidents without police reports, ensuring all parties involved are documented.