Fill Out a Valid Nevada Modified Tax Return Template

Fill Out a Valid Nevada Modified Tax Return Template

In the realm of Nevada's business operations, staying compliant with tax obligations is paramount for all enterprises, big and small. At the core of these obligations is the Nevada Modified Business Tax Return, a crucial document that encapsulates the financial responsibilities businesses have towards the state. Officially revised in 2016 and issued by the Nevada Department of Taxation, this form serves as a comprehensive tool for businesses to report their quarterly gross wages, including tips. What makes this form unique is its consideration for deductions ranging from employer-paid health care costs to wages paid to qualified veterans, ensuring businesses are taxed fairly. It includes detailed calculations for determining taxable wages, applying the $50,000 threshold set by SB483, and calculating the amount of tax due after accounting for various credits such as the Commerce Tax credit and other approved credits. The form also outlines penalties and interest applicable for late submissions, emphasizing the importance of timeliness in fulfilling tax obligations. Designed with specificity for general businesses, excluding financial institutions which use a different form, it is a key piece of documentation for maintaining compliance and ensuring that businesses contribute their fair share to Nevada's economy. For those navigating through the complexities of business taxation in Nevada, understanding and accurately completing the Modified Business Tax Return is a critical step in securing a business’s good standing and financial health.

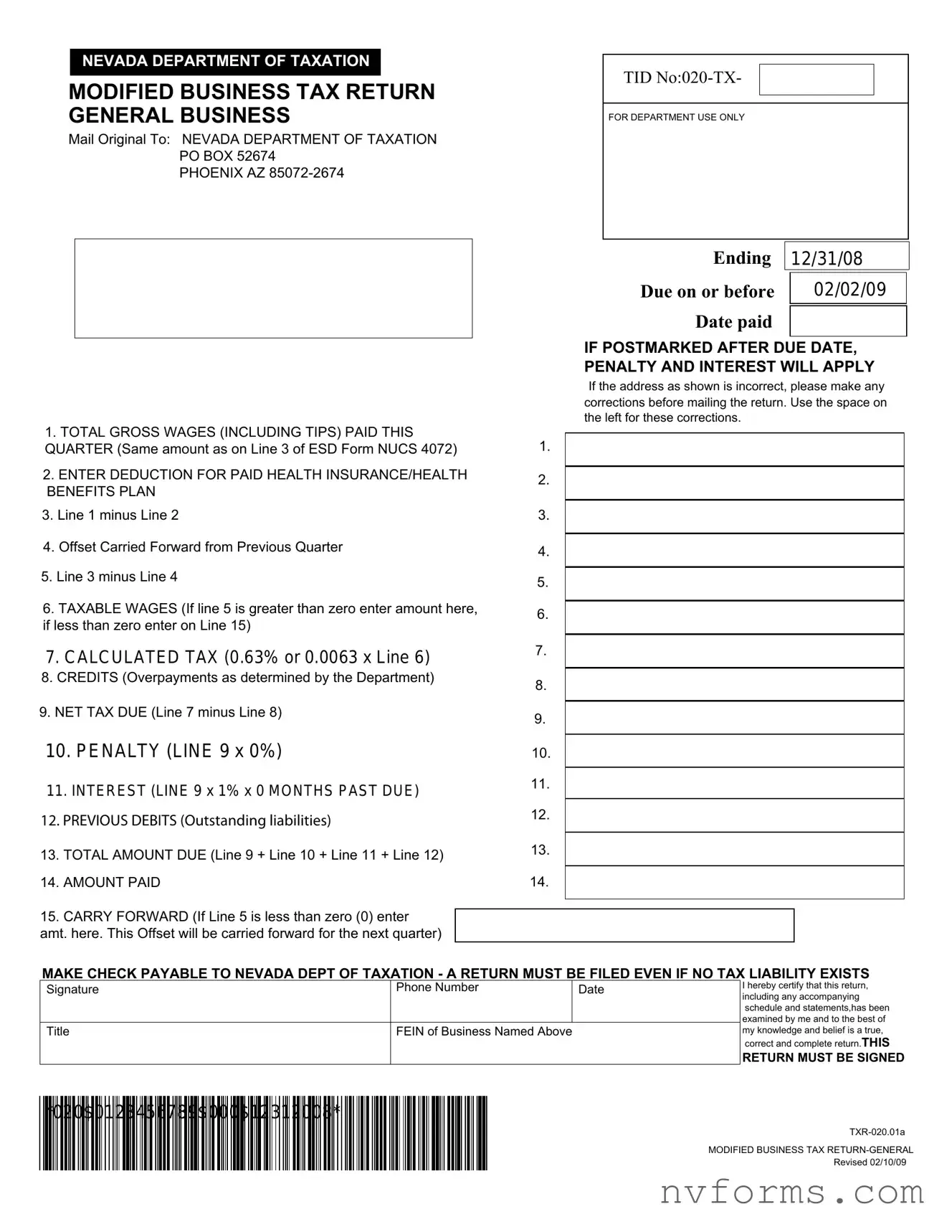

NEVADA DEPARTMENT OF TAXATION

MODIFIED BUSINESS TAX RETURN GENERAL BUSINESS

Mail Original To: NEVADA DEPARTMENT OF TAXATION PO BOX 52674

PHOENIX AZ

TID

FOR DEPARTMENT USE ONLY

Ending |

12/31/08 |

|

|

|

|

Due on or before |

|

02/02/09 |

Date paid |

|

|

|

|

|

|

|

|

IF POSTMARKED AFTER DUE DATE, PENALTY AND INTEREST WILL APPLY

If the address as shown is incorrect, please make any corrections before mailing the return. Use the space on the left for these corrections.

1.TOTAL GROSS WAGES (INCLUDING TIPS) PAID THIS QUARTER (Same amount as on Line 3 of ESD Form NUCS 4072)

2.ENTER DEDUCTION FOR PAID HEALTH INSURANCE/HEALTH BENEFITS PLAN

3.Line 1 minus Line 2

4.Offset Carried Forward from Previous Quarter

5.Line 3 minus Line 4

6.TAXABLE WAGES (If line 5 is greater than zero enter amount here, if less than zero enter on Line 15)

7.CALCULATED TAX (0.63% or 0.0063 x Line 6)

8.CREDITS (Overpayments as determined by the Department)

9.NET TAX DUE (Line 7 minus Line 8)

10.PENALTY (LINE 9 x 0%)

11.INTEREST (LINE 9 x 1% x 0 MONTHS PAST DUE)

12.PREVIOUS DEBITS (Outstanding liabilities)

13.TOTAL AMOUNT DUE (Line 9 + Line 10 + Line 11 + Line 12)

14.AMOUNT PAID

15.CARRY FORWARD (If Line 5 is less than zero (0) enter

amt. here. This Offset will be carried forward for the next quarter)

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

MAKE CHECK PAYABLE TO NEVADA DEPT OF TAXATION - A RETURN MUST BE FILED EVEN IF NO TAX LIABILITY EXISTS

Signature

Title

Phone Number |

Date |

|

|

FEIN of Business Named Above

I hereby certify that this return, including any accompanying schedule and statements,has been examined by me and to the best of my knowledge and belief is a true,

correct and complete return.THIS

RETURN MUST BE SIGNED

*020$0123456789$000$12312008*

MODIFIED BUSINESS TAX

Revised 02/10/09

INSTRUCTIONS - MODIFIED BUSINESS TAX RETURN - GENERAL BUSINESSES ONLY (Financial

Institutions need to use the form developed specifically for them,

Line 1. Total Gross Wages - Enter the total amount of all gross wages and reported tips paid this calendar quarter. (Same amount as on Line 3 of ESD Form NUCS 4072.) DO NOT include a copy of NUCS 4072 with this return.

Line 2. Employer paid health care costs, paid this calendar quarter, as described in NRS 363B.110. Line 3. Line 1 minus Line 2.

Line 4. Offsets carried forward are created when allowable health care costs exceed gross wages in the previous quarter. If applicable, enter the previous quarter's offset here. This is not a credit against any tax due. This reduces the wage base upon which the tax is calculated.

Line 5. Line 3 minus Line 4.

Line 6. Taxable wages is the amount that will be used in the calculation of the tax. If line 5 is greater than zero, this is the taxable wages. If line 5 is less than zero, then no tax is due. (This amount will be entered on line 15 as the offset carried forward for the next quarter.)

Line 7. Calculate Tax Due - Taxable wages x (rate shown on line 7) = the tax due. (Rate Varies by Period End Date according to Tax Laws)

Line 8. Credits - Enter amount of overpayment of Modified Business Tax made in prior reporting periods for which you have received a Department of Taxation credit notice. Do not take the credit if you have applied for a refund. NOTE: Only credits established by the Department may be used.

Line 9. Net Tax Due - Line 7 minus Line 8. This amount is due and payable by the due date; the last day of the month following the applicable quarter. If payment of the tax is late, penalty and interest (as calculated below) are applicable.

LINE 10- If this return is not submitted/postmarked and taxes are not paid on or before the due date as shown on the face of this return, the amount of penalty due is: a) For returns with Period(s) Ending prior to and including 3/31/07 the Penalty is 10%; b) For returns with Period(s) Ending 4/30/07 and after; the amount of penalty due is based on the number of days the payment is late per NAC 360.395 (see table below). The maximum penalty amount is 10%.

Number of days late |

Penalty Percentage |

Multiply by: |

1 - 10 |

2% |

0.02 |

11 - 15 |

4% |

0.04 |

16 - 20 |

6% |

0.06 |

21- 30 |

8% |

0.08 |

31 + |

10% |

0.10 |

Line 11. Interest - If this return will not be postmarked and the taxes paid on or before the applicable due date, enter 1% (0.01) x (times) line 9 for each month or fraction of a month late.

Line 12. Previous Debits - Enter only those liabilities that have been established for prior quarters by the Department and for which you have received a liability notice.

Line 13. Total Amount Due

Line 14. Amount Paid - Enter the amount remitted with return.

Line 15. Carry Forward - If line 5 is less than zero enter figure here. This amount will be carried forward to the next quarter (offset).

GENERAL INFORMATION:

GENERAL BUSINESSES MUST USE FORM

Who Must File: Every employer who is subject to the Nevada Unemployment Compensation Law (NRS 612) except for

A copy of the form NUCS 4072, as filed with Nevada Employment Security Division, does not need to be included with the original return, but should be available upon request by the Department.

Businesses that have ceased doing business (gone out of business) in Nevada must notify the Employment Security Division and the Department of Taxation in writing, the date the business ceased doing business.

AMENDING RETURN(S):

1.Copy of the original return.

2.The word "AMENDED" written in black in the upper

3.

4.Enter corrected figures, in black, next to/above

5. Enter amount of credit claimed (if any) or amount due.

6.Include a WRITTEN EXPLANATION AND DOCUMENTATION (credit memos, exemption certificates, adjustments to gross wages or health care deductions, etc.) substantiating the basis of the amendment(s).

7.If the amended return results in a credit, a credit will be issued to satisfy current /future liabilities unless a refund is specifically requested.

8.If additional tax is due, please remit payment along with applicable penalty and interest.

The Department will send written notice when a credit request has been processed and the credit is available for use/refund.

Please do not use/apply a credit prior to receiving Departmental notification that it is available.

| Fact | Detail |

|---|---|

| Form Title | Nevada Modified Business Tax Return |

| Revision Date | June 21, 2016 |

| Applicable To | General Businesses (Specific form available for Financial Institutions) |

| Governing Law | NRS 363B.115, SB 483, AB 71 of the 78th (2015) Legislative Session |

| Submission Method | Mail or Email |

| Main Components | Total Gross Wages, Deductions for Paid Health Insurance, Health Benefits and Qualified Veterans' Wages, Net Taxable Wages, Tax Calculations, Credits, and Penalties/Interest |

| Tax Rate | Calculated Tax is based on Line 8 x 0.01475 |

| Credits Inclusion | Commerce Tax Credit and Other Approved Credits |

Filing the Nevada Modified Business Tax Return requires careful attention to detail and adherence to specific instructions provided by the Nevada Department of Taxation. This document is essential for businesses operating within Nevada, as it helps in the calculation and payment of taxes due based on wages paid during a specific quarter. The process involves including wages, deductions for health insurance and qualified veterans' wages, and any applicable credits or offsets. Entities must ensure accuracy in their reporting to avoid potential penalties or interest owing to incorrect filings. Below is a step-by-step guide that outlines the necessary steps in completing this form.

After completing the form, it should be mailed to the Nevada Department of Taxation at the address provided or emailed as an attachment to the specified address. It is crucial for businesses to comply with the deadlines to avoid penalties and interest for late filing or payment. This tax return form is a necessary document for maintaining compliance with Nevada's tax laws for businesses.

Filling out tax forms accurately is crucial for compliance and financial efficiency, particularly for businesses navigating the complexities of state tax obligations. In Nevada, the Modified Business Tax (MBT) Return is a critical document requiring careful attention to detail. Businesses commonly make several mistakes when completing this form, which can lead to unintended consequences, including penalties, interest charges, or incorrect tax liabilities. Here, we elucidate seven common errors to avoid.

To navigate these pitfalls, thorough review and understanding of the MBT Return instructions are indispensable. Accuracy in reporting, diligent calculation, and attentive adherence to the guidelines will mitigate risks associated with these common errors. Engaging a professional for guidance or clarification when in doubt can further ensure compliance and financial accuracy for businesses operating in Nevada.

When businesses in Nevada prepare their Modified Business Tax Return, there are several other documents and forms that they often need to complete or have on hand. These additional documents ensure compliance with Nevada's tax laws and facilitate accurate tax reporting. Let's delve into four of these commonly used documents.

Each of these documents plays a crucial role in the tax filing process for businesses operating in Nevada. By thoroughly preparing and accurately completing these forms, businesses can ensure they meet their tax obligations, take advantage of applicable credits, and maintain compliance with state tax regulations.

The Nevada Modified Tax Return form is similar to several key documents used in business taxation, each for its unique purpose and structure. Understanding these similarities helps in accurately preparing and filing taxes, ensuring compliance with the respective guidelines and regulations.

Firstly, the form echoes the structure of the Federal Unemployment Tax Act (FUTA) Tax Return, which employers submit to report federally mandated unemployment taxes. Like the Nevada Modified Tax Return, the FUTA Tax Return requires detailed wage information, distinguishing between total gross wages and those subject to taxation after deductions and exemptions. However, FUTA focuses on federal unemployment contributions rather than the broader scope of state business taxes and does not include deductions for things like paid health insurance or benefits for hiring veterans.

Secondly, it shares similarities with the Internal Revenue Service (IRS) Form 941, Employer's Quarterly Federal Tax Return. This form is used to report income taxes, social security tax, or Medicare tax withheld from employees' paychecks, and to pay the employer's portion of social security or Medicare tax. The Nevada Modified Tax Return and IRS Form 941 both require employers to calculate taxes based on wages paid, albeit for different types of taxes. Furthermore, both forms allow for adjustments to tax calculations for specific credits or offsets, such as the healthcare deduction or the Commerce Tax credit in the case of the Nevada form.

Lastly, it is analogous to state-specific workers' compensation insurance premium forms, which businesses use to report wages to state agencies for the calculation of insurance premiums. These forms, like the Nevada Modified Tax Return, rely on detailed wage reporting and allow for certain reductions based on specific types of employee benefits or programs. However, workers' compensation forms are strictly for the purpose of calculating insurance premiums, not for business taxation.

Each of these documents, while unique in its focus and application, shares the fundamental requirement of reporting wage and payroll information for the purpose of calculating and reporting taxes or premiums. The Nevada Modified Tax Return integrates aspects of federal and state tax reporting, emphasizing the importance of comprehensive and accurate wage reporting as the foundation of business taxation and compliance.

When filling out the Nevada Modified Tax Return form, there are several dos and don'ts that businesses should keep in mind to ensure the process goes smoothly and accurately. Here is a list of things you should and shouldn't do:

Understanding the Nevada Modified Business Tax Return form can be challenging, and there are several common misconceptions associated with it. Let's clarify these misconceptions to aid in accurate and efficient tax filing.

In fact, every employer subject to the Nevada Unemployment Compensation Law, with few exceptions (such as non-profit 501(c) organizations, Indian tribes, and political subdivisions), must file this return. Size doesn't exempt a business from filing.

While reporting total gross wages is a primary component, the form also includes sections for deductions like paid health insurance and qualified veterans' wages, and other credits and adjustments. It covers more than just wages.

Overpayments are subject to approval and must be documented by a credit notice from the Department of Taxation. They're not automatically rolled over to the next period without proper authorization.

This credit is indeed equal to 50% of the Commerce Tax paid in the prior year but is only applicable up to the amount of Modified Business Tax owed. Excess credit may be carried forward, subject to limitations.

Taxable wages are calculated by subtracting certain allowed deductions and offsets from the total gross wages. Not all wages paid will be subject to tax after these deductions.

Penalties are based on how late the payment is, with rates increasing the longer the delay. Similarly, interest is calculated as a percentage for each month the payment is overdue.

While emailing the return is an option, businesses can also mail the original document to the Nevada Department of Taxation. Choosing the best method depends on the filer's preference and convenience.

Even if no liability exists, the form explicitly states that a return must be filed. Filing a return with no tax due is still a legal requirement.

Understanding these misconceptions helps ensure accurate completion and timely submission of the Nevada Modified Business Tax Return, avoiding potential penalties and fostering compliance with state taxation laws.

Filing the Nevada Modified Business Tax Return requires attention to detail and an understanding of the specific deductions and credits available to businesses. Here are seven key takeaways that can guide you through the process:

Each of these elements plays a crucial role in accurately completing the Nevada Modified Business Tax Return. By paying attention to the specific deductions, credits, and thresholds, businesses can ensure they're not overpaying their taxes while remaining compliant with state tax laws.

What Qualifies You for a Handicap Placard - If a vehicle's emission standards compliance was proven over 90 days ago, re-inspection may be necessary before registration, as noted in the SP41 form instructions.

Nevada Title - Used by highway and off-highway vehicle dealers to apply for a sales report extension.

Nred - Illustrates the procedure for Nevada community associations with fewer than 20 units in specific counties to have reserve studies conducted by a qualified individual.