Fill Out a Valid Nevada Sales Tax Template

Fill Out a Valid Nevada Sales Tax Template

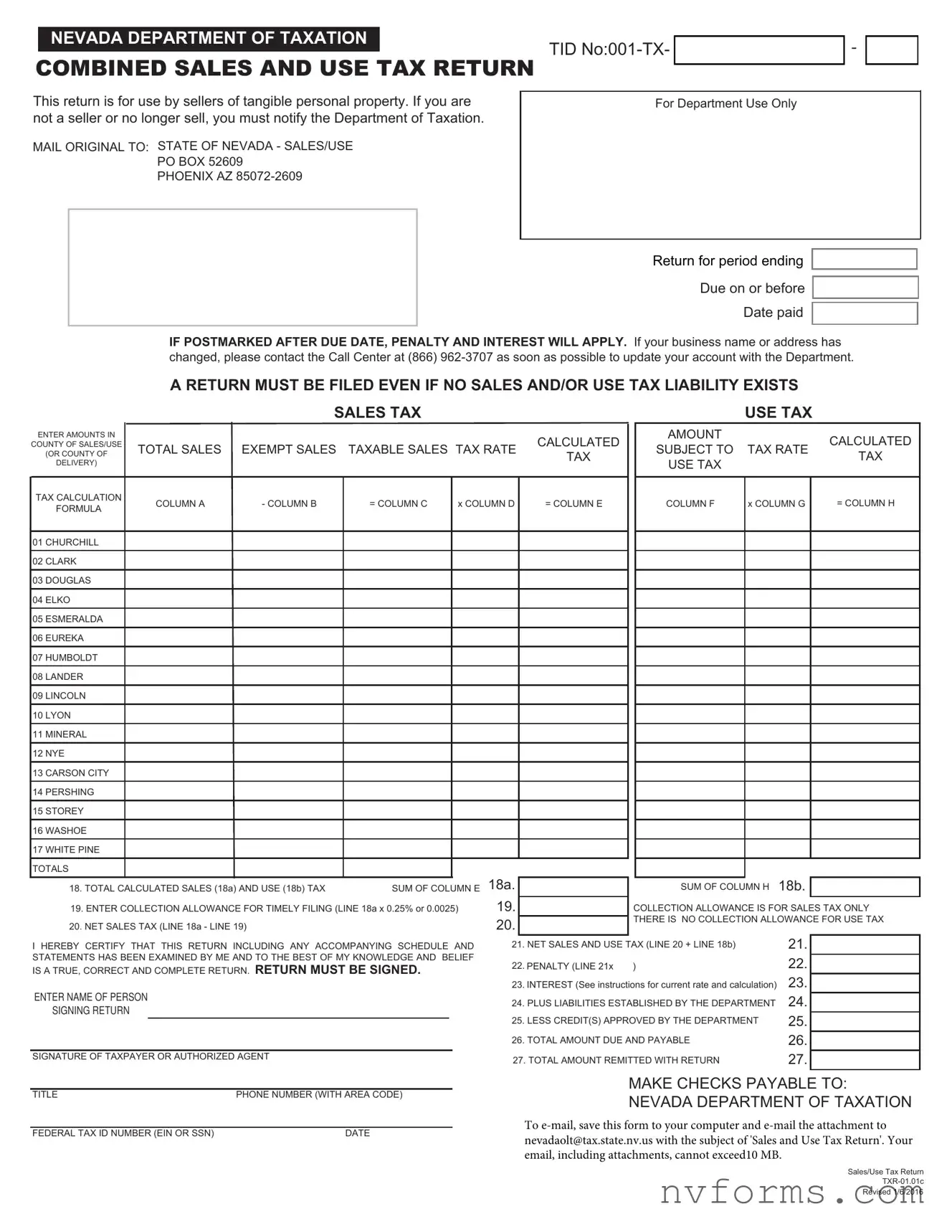

The Nevada Sales Tax form, as provided by the Nevada Department of Taxation, serves as a critical document for sellers of tangible personal property within the state. This comprehensive form, designated for combined sales and use tax return purposes, mandates sellers to meticulously report sales transactions and calculate the taxes owed accordingly. Its structure facilitates the differentiation between taxable and exempt sales, ensuring that businesses accurately determine their tax liabilities based on the varying tax rates applicable across different counties. Important aspects such as penalties and interest for late submissions are delineated, underscoring the importance of timeliness and accuracy in filing. Furthermore, the form accommodates adjustments through collection allowances for timely filings, credits for overpayments, and deductions for any liabilities established by the department. The meticulous completion of this form, including signature verification and rightful submission to the specified mailing address, is essential for compliance. Moreover, it carries a stern reminder that a return must be filed even in the absence of sales or use tax liability, emphasizing the department's commitment to maintaining updated records of all business activities related to the sale of tangible personal property in Nevada.

NEVADA DEPARTMENT OF TAXATION

TID

COMBINED SALES AND USE TAX RETURN

-

This return is for use by sellers of tangible personal property. If you are not a seller or no longer sell, you must notify the Department of Taxation.

MAIL ORIGINAL TO: STATE OF NEVADA - SALES/USE

PO BOX 52609

PHOENIX AZ

For Department Use Only

Return for period ending

Due on or before

Date paid

IF POSTMARKED AFTER DUE DATE, PENALTY AND INTEREST WILL APPLY. If your business name or address has changed, please contact the Call Center at (866)

|

|

|

A RETURN MUST BE FILED EVEN IF NO SALES AND/OR USE TAX LIABILITY EXISTS |

|

|||||||||||||

|

|

|

|

SALES TAX |

|

|

|

|

|

|

|

USE TAX |

|

||||

ENTER AMOUNTS IN |

|

|

|

|

|

|

|

|

|

CALCULATED |

|

|

AMOUNT |

|

|

|

CALCULATED |

COUNTY OF SALES/USE |

|

TOTAL SALES |

EXEMPT SALES |

TAXABLE SALES TAX RATE |

|

|

SUBJECT TO |

TAX RATE |

|||||||||

(OR COUNTY OF |

|

TAX |

|

|

TAX |

||||||||||||

DELIVERY) |

|

|

|

|

|

|

|

|

|

|

|

USE TAX |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TAX CALCULATION |

|

|

COLUMN A |

- COLUMN B |

= COLUMN C |

x COLUMN D |

|

= COLUMN E |

|

|

COLUMN F |

x COLUMN G |

|

= COLUMN H |

|||

FORMULA |

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

01 CHURCHILL |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

02 CLARK |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

03 DOUGLAS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

04 ELKO |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

05 ESMERALDA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

06 EUREKA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

07 HUMBOLDT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

08 LANDER |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

09 LINCOLN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10 LYON |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11 MINERAL |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12 NYE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13 CARSON CITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 PERSHING |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15 STOREY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16 WASHOE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17 WHITE PINE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTALS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18a. |

|

|

|

|

|

|

18b. |

|

|

||

18. TOTAL CALCULATED SALES (18a) AND USE (18b) TAX |

SUM OF COLUMN E |

|

|

|

|

SUM OF COLUMN H |

|

|

|||||||||

|

|

|

|

|

|

19. |

|

|

|

|

|

|

|||||

19. ENTER COLLECTION ALLOWANCE FOR TIMELY FILING (LINE 18a x 0.25% or 0.0025) |

|

|

|

COLLECTION ALLOWANCE IS FOR SALES TAX ONLY |

|||||||||||||

20. NET SALES TAX (LINE 18a - LINE 19) |

|

|

|

20. |

|

|

|

THERE IS NO COLLECTION ALLOWANCE FOR USE TAX |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

I HEREBY CERTIFY THAT THIS RETURN INCLUDING ANY ACCOMPANYING SCHEDULE AND |

21. NET SALES AND USE TAX (LINE 20 + LINE 18b) |

|

21. |

|

|

||||||||||||

STATEMENTS HAS BEEN EXAMINED BY ME AND TO THE BEST OF MY KNOWLEDGE AND BELIEF |

22. |

PENALTY (LINE 21x |

) |

|

|

22. |

|

|

|||||||||

IS A TRUE, CORRECT AND COMPLETE RETURN. RETURN MUST BE SIGNED. |

|

|

|

|

|

||||||||||||

|

23. INTEREST (See instructions for current rate and calculation) |

23. |

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||

ENTER NAME OF PERSON |

|

|

|

|

24. PLUS LIABILITIES ESTABLISHED BY THE DEPARTMENT |

24. |

|

|

|||||||||

SIGNING RETURN |

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

25. LESS CREDIT(S) APPROVED BY THE DEPARTMENT |

25. |

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

26. TOTAL AMOUNT DUE AND PAYABLE |

|

26. |

|

|

|||||

SIGNATURE OF TAXPAYER OR AUTHORIZED AGENT |

|

|

|

27. TOTAL AMOUNT REMITTED WITH RETURN |

|

27. |

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

TITLE |

PHONE NUMBER (WITH AREA CODE) |

|

|

FEDERAL TAX ID NUMBER (EIN OR SSN) |

DATE |

MAKE CHECKS PAYABLE TO:

NEVADA DEPARTMENT OF TAXATION

To

Sales/Use Tax Return

Revised 1/6/2016

COMBINED SALES AND USE TAX RETURN INSTRUCTIONS

This return is for use by sellers of tangible personal property registered with the Department

A RETURN MUST BE FILED EVEN IF NO TAX LIABILITY EXISTS

LINES 1 THROUGH 17

COLUMN A: TOTAL SALES - On the appropriate county line, enter the amount of all sales (excluding the sales tax collected) related to Nevada business including (a) cash sales; (b) conditional sales; (c) sales exempt from tax.

COLUMN B: EXEMPT SALES - Enter that portion of your sales not subject to tax, i.e., sales (a) for which you receive a resale certificate; (b) to Federal Government, State of Nevada, its agencies, cities or counties and school districts; (c) to religious or charitable organizations for which you have copies of exemption letters on file; (d) newspapers of general circulation published at least once a week; (e) animals, seeds, annual plants and fertilizer, the end product of which is food for human consumption; (f) motor vehicle or special fuels used in internal combustion or diesel engines; (g) wood, presto logs, pellets, petroleum, gas and any other matter used to produce domestic heat and sold for home or household use; (h) prescription medicines dispensed pursuant to a prescription by a licensed physician, dentist or chiropodist; (i) food products sold for home preparation and consumption; (j)

.

COLUMN C: TAXABLE SALES - Total Sales (Column A) - Exempt Sales (Column B) = Taxable Sales (Column C).

COLUMN E: CALCULATED TAX - Taxable Sales (Column C) × Tax Rate (Column D) = Calculated Tax (Column E).

COLUMN F: AMOUNT SUBJECT TO USE TAX - On the appropriate county line, enter (a) the purchase price of merchandise, equipment or other tangible personal property purchased without payment of Nevada tax (by use of your resale certificate, or any other reason) and that was stored, used or consumed by you rather than being resold. NOTE: If you have a contract exemption, give contract exemption number.

COLUMN H: CALCULATED TAX - Amount Subject to Use Tax (Column F) × Tax Rate (Column G) = Calculated Tax (Column H).

LINE 18A Enter the total of Column E.

LINE 18B Enter the total of Column H.

LINE 19 Take the Collection Allowance only if the return and taxes are postmarked on or before the due date as shown on the face of this return. If not postmarked by the due date, the Collection Allowance is not allowed. To calculate the Collection Allowance multiply Line 18a × 0.25% (or .0025). NOTE: Pursuant to NRS 372.370, the Collection Allowance is applicable to Sales Tax only.

LINE 20 Subtract Line 19 from Line 18a and enter the result.

LINE 21 Add Line 20 to Line 18b and enter the result.

LINE 22 If this return is not submitted/postmarked and taxes are not paid on or before the due date as shown on the face of this return, the amount of penalty due is based on the number of days the payment is late per NAC 360.395 (see table below). The maximum penalty amount is 10%.

Number of days late |

Penalty Percentage |

Multiply by: |

|

|

|

1 - 10 |

2% |

0.02 |

|

|

|

11 - 15 |

4% |

0.04 |

|

|

|

16 - 20 |

6% |

0.06 |

|

|

|

21- 30 |

8% |

0.08 |

|

|

|

31 + |

10% |

0.10 |

|

|

|

Determine the number of days late the payment is, and multiply the net tax owed (Line 21) by the appropriate rate based on the table to the left. The result is the amount of penalty that should be entered. For example, if the taxes were due January 31, but not paid until February 15. The number of days late is 15 so the penalty is 4%. The penalty and interest amounts are automatically calculated for you if this form is completed on your computer.

LINE 23 To calculate interest, multiply Line 21 x 0.75% (or .0075) for each month payment is late.

LINE 24 Enter any amount due for prior reporting periods for which you have received a Department of Taxation billing notice.

LINE 25 Enter amount due to you for overpayment made in prior reporting periods for which you have received a Department of Taxation credit notice. Do not take the credit if you have applied for a refund. NOTE: Only credits established by the Department may be used.

LINE 26 Add Lines 21, 22, 23, 24 and then subtract Line 25 and enter the result.

LINE 27 Enter the total amount paid with this return.

Complete and detailed records of all sales, as well as income from all sources and expenditures for all purposes, must be kept so your return can be verified by a Department auditor.

YOU MUST COMPLETE THE SIGNATURE PORTION BY TYPING IN THE NAME OF THE PERSON SIGNING THE RETURN AND MAIL TO: Nevada Department of Taxation, PO Box 52609, Phoenix, AZ

local office.

DO NOT SUBMIT A PHOTOCOPY OF A PRIOR PERIOD FORM, YOUR FILING WILL POST INCORRECTLY.

If you have questions concerning this return, please call our Department's Call Center at (866)

SALES/USE TAX RETURN INSTRUCTIONS

Revised 01/04/2016

| Fact | Detail |

|---|---|

| Governing Law | NRS 372.370 and NAC 360.395 govern the application, penalty, and interest calculations on the Nevada Combined Sales and Use Tax Return. |

| Form Purpose | The form is designed for sellers of tangible personal property to report and remit sales and use taxes collected. |

| Mandatory Filing | A return must be filed even if no sales and/or use tax liability exists. |

| Due Date | The due date is based on the return period ending date, and penalties and interest apply if the return is postmarked after this date. |

| Penalty Calculation | Penalties are calculated based on the number of days late, with a maximum penalty of 10% as per NAC 360.395. |

| Interest Calculation | Interest is calculated at a rate of 0.75% per month (or .0075) for each month the payment is late. |

| Signature Required | The return must be signed by the taxpayer or an authorized agent to certify the accuracy of the information provided. |

| Collection Allowance | A 0.25% (or .0025) collection allowance is available for sales tax only, provided the return and payment are postmarked by the due date. |

Filing the Nevada Sales Tax form is a straightforward process designed for sellers of tangible personal property. The form ensures that the appropriate sales and use taxes are collected and reported to the Nevada Department of Taxation. It's essential to provide accurate information to avoid any penalties and interest for late or incorrect filings. Before starting, gather all necessary sales records and ensure you understand the tax rates applicable to your sales and use scenarios. Follow the steps below to complete the form properly.

Ensure your form is complete and accurate before submission. Keep a copy of all documents for your records. Timely and accurate filing will help avoid potential penalties and interest charges.

What should I do if my business name or address has changed since my last Nevada Sales Tax filing?

If your business name or address has changed, it's important to update your account information with the Nevada Department of Taxation as soon as possible. You can do this by contacting the Call Center at (866) 962-3707. Keeping your information up to date ensures that you receive all necessary communications and helps prevent any issues with your tax filings.

Do I have to file a Nevada Sales Tax return even if I did not make any sales or owe any sales tax?

Yes, you are required to file a return for every period, even if you did not have any taxable sales or owe any sales and use tax. Failing to file can result in penalties and interest charges. It’s important to complete and submit your return to comply with Nevada tax laws, confirming that you had no tax liability for the period.

How is the Collection Allowance calculated on the Nevada Sales Tax form?

The Collection Allowance is provided as an incentive for timely filing and payment of the sales tax. To calculate the allowance, multiply Line 18a (the total calculated sales tax) by 0.25% (or .0025). Note that this allowance applies only to sales tax, not use tax. Moreover, to be eligible for this deduction, your return and payment must be postmarked on or before the due date indicated on the sales tax form.

What happens if I file or pay my Nevada Sales Tax late?

If your Nevada Sales Tax return is filed or paid after the due date, penalties and interest will apply. The penalty is calculated based on the amount of tax owed and the number of days the payment is late, with rates ranging from 2% to 10% of the net tax due. Additionally, interest is charged at a rate of 0.75% (.0075) for each month the payment is late. It's essential to file and pay on time to avoid these extra charges.

When completing the Nevada Sales Tax form, individuals often make mistakes that can lead to inaccuracies or delays in processing. Understanding these common errors can help ensure that the forms are filled out correctly and efficiently.

One of the first mistakes is not updating business information. Businesses evolve, and changes such as a new address or business name need to be communicated to the Nevada Department of Taxation as soon as possible. This information is crucial for communication and to avoid misdirected correspondence.

In summary, filling out the Nevada Sales Tax form accurately requires attention to detail and an understanding of the specific requirements. By avoiding common mistakes, such as incorrect calculations, overlooking exemptions, missing deadlines, not claiming allowances, and submission errors, individuals can improve the accuracy and efficiency of their tax filings.

Filing the Nevada Sales and Use Tax Return is a critical step for businesses operating within the state, ensuring compliance with local tax laws by reporting sales, use, and taxable transactions. However, this form is just one part of a broader suite of documents and forms that businesses may need to manage their tax responsibilities effectively. Understanding these additional documents can provide a clearer picture of a business's fiscal duties and assist in maintaining accurate records for both state and federal tax purposes.

Together, these documents encompass a vital framework for managing and reporting a business's tax-related activities in Nevada. By staying informed and compliant with these requirements, businesses can ensure they meet their legal obligations and contribute to Nevada's economic health. Ensuring accuracy and timeliness in all tax matters, from sales and use tax to employee wages, plays a crucial role in the smooth operation of any business within the state.

The Nevada Sales Tax form is similar to other tax forms used by businesses and individuals to calculate and report their liabilities to government agencies. Understanding how this form compares to others offers insight into the broader framework of tax reporting and compliance. Each document has its own purpose, but the method of reporting financial activities shares common ground across various forms.

IRS Form 1040, the U.S. Individual Income Tax Return, shares a fundamental similarity with the Nevada Sales Tax form in that both require detailed financial reporting. The 1040 form is used to report an individual's annual income and calculate taxes owed to the federal government. Like the Nevada Sales Tax form, it includes sections for calculating taxable income, deductions, credits, and the resulting tax liability. Both forms require the taxpayer to certify the accuracy of the information provided under penalty of perjury. While the 1040 form focuses on personal income and the Nevada form on taxable sales and use, they similarly structure the process of declaring financial activities, calculating owed amounts, and facilitating compliance with tax laws.

Form 1120, the U.S. Corporation Income Tax Return, is another document that resembles the Nevada Sales Tax form in its purpose and structure. It is designed for corporations to report their annual income, gains, losses, deductions, and to calculate the federal income tax liability. Both the Nevada Sales Tax form and Form 1120 include detailed instructions on income reporting and tax calculations, offer schedules for various types of deductions and credits, and require the submission of additional documents or schedules for specific reporting needs. They serve a critical function in aligning business operations with tax responsibilities, ensuring that the correct amount of tax is calculated and paid to the respective tax authority.

Schedule C (Form 1040), Profit or Loss From Business, is particularly relevant to individuals who operate a sole proprietorship or single-member LLC. This form requires the taxpayer to detail the income and expenses of their business, much like how the Nevada Sales Due form requires businesses to report sales, exemptions, and taxable amount. Both forms are crucial for financial accountability, allowing for the calculation of net profit or loss which directly affects tax liability. The active detailing of financial operations in both forms underscores their importance in tax planning and compliance for business activities.

When completing the Nevada Sales Tax form, it's crucial to observe both the dos and don'ts to ensure accuracy and compliance. Here are essential pointers to guide you through this process:

Do:

Don't:

Understanding the Nevada Sales Tax form and its requirements can be complex, leading to several misconceptions within the business community. Here are eight common misunderstandings and the facts that clarify them:

Fact: Regardless of whether a business has taxable sales or not, a return must be filed for each period. This ensures compliance and updates the Nevada Department of Taxation on the business's status.

Fact: The collection allowance, calculated as 0.25% of the total sales tax due, only applies to sales tax. There is no collection allowance for use tax.

Fact: Use tax must be accounted for on all tangible personal property purchased without paying Nevada sales tax. This includes not only large purchases but also small, everyday items if they are used, stored, or consumed in Nevada.

Fact: While out-of-state sales may be exempt from Nevada sales tax, they must be properly documented and meet specific criteria to qualify for this exemption.

Fact: Electronic filing does not exempt a business from late penalties and interest. Timeliness and accuracy when filing are crucial, regardless of the method used.

Fact: Nevada sales tax rates vary by county. It's crucial to apply the correct tax rate when calculating sales tax due for transactions in specific counties.

Fact: Penalties for late filing are calculated based on the number of days the payment is late and can vary widely. They can range from 2% to 10% of the net tax owed, depending on how late the payment is made.

Fact: While the return is primarily designed for sellers of tangible personal property, it may apply to other entities based on their activities and tax liabilities in Nevada. Consulting with the Department of Taxation can clarify specific obligations.

Clarifying these misconceptions helps ensure that businesses can better comply with Nevada's sales and use tax regulations, avoiding unnecessary penalties and interest. Always seek current information directly from the Nevada Department of Taxation or a professional tax advisor to stay informed on tax obligations and updates.

Filling out the Nevada Sales and Use Tax Return correctly is crucial for businesses to comply with state regulations. Here are six key takeaways to ensure accuracy and avoid common pitfalls:

Adhering to these guidelines when completing the Nevada Sales and Use Tax Return will help ensure compliance, minimize errors, and avoid unnecessary penalties. For further assistance or clarification, it is advisable to contact the Nevada Department of Taxation or a tax professional.

Nevada Medicaid Provider Portal - Having a designated fax number for the FA-29 form submission streamlines the correction process, facilitating quicker administrative resolutions.

Welfare Application Form - The form inquires about any accidents that might affect medical benefits or insurance claims for the household members.