Fill Out a Valid State Nevada Tax Template

Fill Out a Valid State Nevada Tax Template

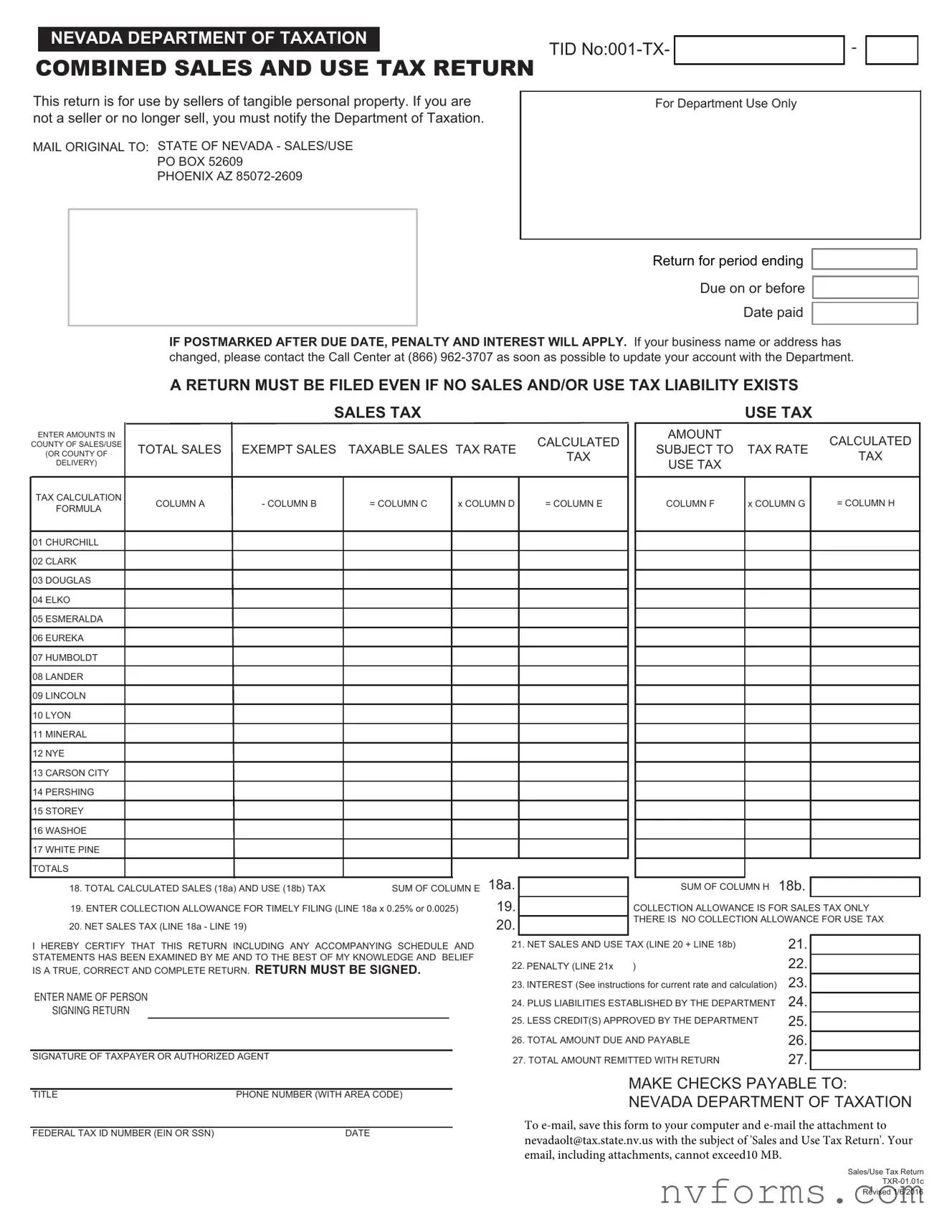

The State Nevada Tax form, as issued by the Nevada Department of Taxation, serves a crucial role for sellers of tangible personal property within the state, outlining a comprehensive procedure for the reporting and remission of both sales and use taxes. Executors of these forms are engaged in a meticulous process that begins with the disclosure of total sales, exempt sales, and subsequently, taxable sales, following through to the exact calculations of taxes due, based on rates that vary by county. Noteworthy is the provision allowing for a collection allowance for those who file timely, essentially offering a slight reduction in the sum owed. Penalties and interest charges, as delineated in this document, stand as a deterrent against late filings, encouraging adherence to stipulated deadlines. This document also accommodates updates for personal or business information changes, thus ensuring that records held by the Department are current. Furthermore, it mandates that a return must be filed irrespective of a business’s tax liability for the period in question, emphasizing the state’s diligence in maintaining up-to-date financial records. The form’s layout, which includes a signature section, certifies the accuracy and completeness of the information provided by the taxpayer or an authorized agent, underpinning the legal importance of this declaration. In essence, the Combined Sales and Use Tax Return form is a critical instrument for both the state and its business constituents, facilitating the organized collection of taxes essential for public and state-funded projects.

NEVADA DEPARTMENT OF TAXATION

TID

COMBINED SALES AND USE TAX RETURN

-

This return is for use by sellers of tangible personal property. If you are not a seller or no longer sell, you must notify the Department of Taxation.

MAIL ORIGINAL TO: STATE OF NEVADA - SALES/USE

PO BOX 52609

PHOENIX AZ

For Department Use Only

Return for period ending

Due on or before

Date paid

IF POSTMARKED AFTER DUE DATE, PENALTY AND INTEREST WILL APPLY. If your business name or address has changed, please contact the Call Center at (866)

|

|

|

A RETURN MUST BE FILED EVEN IF NO SALES AND/OR USE TAX LIABILITY EXISTS |

|

|||||||||||||

|

|

|

|

SALES TAX |

|

|

|

|

|

|

|

USE TAX |

|

||||

ENTER AMOUNTS IN |

|

|

|

|

|

|

|

|

|

CALCULATED |

|

|

AMOUNT |

|

|

|

CALCULATED |

COUNTY OF SALES/USE |

|

TOTAL SALES |

EXEMPT SALES |

TAXABLE SALES TAX RATE |

|

|

SUBJECT TO |

TAX RATE |

|||||||||

(OR COUNTY OF |

|

TAX |

|

|

TAX |

||||||||||||

DELIVERY) |

|

|

|

|

|

|

|

|

|

|

|

USE TAX |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TAX CALCULATION |

|

|

COLUMN A |

- COLUMN B |

= COLUMN C |

x COLUMN D |

|

= COLUMN E |

|

|

COLUMN F |

x COLUMN G |

|

= COLUMN H |

|||

FORMULA |

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

01 CHURCHILL |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

02 CLARK |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

03 DOUGLAS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

04 ELKO |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

05 ESMERALDA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

06 EUREKA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

07 HUMBOLDT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

08 LANDER |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

09 LINCOLN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10 LYON |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11 MINERAL |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12 NYE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13 CARSON CITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 PERSHING |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15 STOREY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16 WASHOE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17 WHITE PINE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTALS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18a. |

|

|

|

|

|

|

18b. |

|

|

||

18. TOTAL CALCULATED SALES (18a) AND USE (18b) TAX |

SUM OF COLUMN E |

|

|

|

|

SUM OF COLUMN H |

|

|

|||||||||

|

|

|

|

|

|

19. |

|

|

|

|

|

|

|||||

19. ENTER COLLECTION ALLOWANCE FOR TIMELY FILING (LINE 18a x 0.25% or 0.0025) |

|

|

|

COLLECTION ALLOWANCE IS FOR SALES TAX ONLY |

|||||||||||||

20. NET SALES TAX (LINE 18a - LINE 19) |

|

|

|

20. |

|

|

|

THERE IS NO COLLECTION ALLOWANCE FOR USE TAX |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||

I HEREBY CERTIFY THAT THIS RETURN INCLUDING ANY ACCOMPANYING SCHEDULE AND |

21. NET SALES AND USE TAX (LINE 20 + LINE 18b) |

|

21. |

|

|

||||||||||||

STATEMENTS HAS BEEN EXAMINED BY ME AND TO THE BEST OF MY KNOWLEDGE AND BELIEF |

22. |

PENALTY (LINE 21x |

) |

|

|

22. |

|

|

|||||||||

IS A TRUE, CORRECT AND COMPLETE RETURN. RETURN MUST BE SIGNED. |

|

|

|

|

|

||||||||||||

|

23. INTEREST (See instructions for current rate and calculation) |

23. |

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||

ENTER NAME OF PERSON |

|

|

|

|

24. PLUS LIABILITIES ESTABLISHED BY THE DEPARTMENT |

24. |

|

|

|||||||||

SIGNING RETURN |

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

25. LESS CREDIT(S) APPROVED BY THE DEPARTMENT |

25. |

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

26. TOTAL AMOUNT DUE AND PAYABLE |

|

26. |

|

|

|||||

SIGNATURE OF TAXPAYER OR AUTHORIZED AGENT |

|

|

|

27. TOTAL AMOUNT REMITTED WITH RETURN |

|

27. |

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

TITLE |

PHONE NUMBER (WITH AREA CODE) |

|

|

FEDERAL TAX ID NUMBER (EIN OR SSN) |

DATE |

MAKE CHECKS PAYABLE TO:

NEVADA DEPARTMENT OF TAXATION

To

Sales/Use Tax Return

Revised 1/6/2016

COMBINED SALES AND USE TAX RETURN INSTRUCTIONS

This return is for use by sellers of tangible personal property registered with the Department

A RETURN MUST BE FILED EVEN IF NO TAX LIABILITY EXISTS

LINES 1 THROUGH 17

COLUMN A: TOTAL SALES - On the appropriate county line, enter the amount of all sales (excluding the sales tax collected) related to Nevada business including (a) cash sales; (b) conditional sales; (c) sales exempt from tax.

COLUMN B: EXEMPT SALES - Enter that portion of your sales not subject to tax, i.e., sales (a) for which you receive a resale certificate; (b) to Federal Government, State of Nevada, its agencies, cities or counties and school districts; (c) to religious or charitable organizations for which you have copies of exemption letters on file; (d) newspapers of general circulation published at least once a week; (e) animals, seeds, annual plants and fertilizer, the end product of which is food for human consumption; (f) motor vehicle or special fuels used in internal combustion or diesel engines; (g) wood, presto logs, pellets, petroleum, gas and any other matter used to produce domestic heat and sold for home or household use; (h) prescription medicines dispensed pursuant to a prescription by a licensed physician, dentist or chiropodist; (i) food products sold for home preparation and consumption; (j)

.

COLUMN C: TAXABLE SALES - Total Sales (Column A) - Exempt Sales (Column B) = Taxable Sales (Column C).

COLUMN E: CALCULATED TAX - Taxable Sales (Column C) × Tax Rate (Column D) = Calculated Tax (Column E).

COLUMN F: AMOUNT SUBJECT TO USE TAX - On the appropriate county line, enter (a) the purchase price of merchandise, equipment or other tangible personal property purchased without payment of Nevada tax (by use of your resale certificate, or any other reason) and that was stored, used or consumed by you rather than being resold. NOTE: If you have a contract exemption, give contract exemption number.

COLUMN H: CALCULATED TAX - Amount Subject to Use Tax (Column F) × Tax Rate (Column G) = Calculated Tax (Column H).

LINE 18A Enter the total of Column E.

LINE 18B Enter the total of Column H.

LINE 19 Take the Collection Allowance only if the return and taxes are postmarked on or before the due date as shown on the face of this return. If not postmarked by the due date, the Collection Allowance is not allowed. To calculate the Collection Allowance multiply Line 18a × 0.25% (or .0025). NOTE: Pursuant to NRS 372.370, the Collection Allowance is applicable to Sales Tax only.

LINE 20 Subtract Line 19 from Line 18a and enter the result.

LINE 21 Add Line 20 to Line 18b and enter the result.

LINE 22 If this return is not submitted/postmarked and taxes are not paid on or before the due date as shown on the face of this return, the amount of penalty due is based on the number of days the payment is late per NAC 360.395 (see table below). The maximum penalty amount is 10%.

Number of days late |

Penalty Percentage |

Multiply by: |

|

|

|

1 - 10 |

2% |

0.02 |

|

|

|

11 - 15 |

4% |

0.04 |

|

|

|

16 - 20 |

6% |

0.06 |

|

|

|

21- 30 |

8% |

0.08 |

|

|

|

31 + |

10% |

0.10 |

|

|

|

Determine the number of days late the payment is, and multiply the net tax owed (Line 21) by the appropriate rate based on the table to the left. The result is the amount of penalty that should be entered. For example, if the taxes were due January 31, but not paid until February 15. The number of days late is 15 so the penalty is 4%. The penalty and interest amounts are automatically calculated for you if this form is completed on your computer.

LINE 23 To calculate interest, multiply Line 21 x 0.75% (or .0075) for each month payment is late.

LINE 24 Enter any amount due for prior reporting periods for which you have received a Department of Taxation billing notice.

LINE 25 Enter amount due to you for overpayment made in prior reporting periods for which you have received a Department of Taxation credit notice. Do not take the credit if you have applied for a refund. NOTE: Only credits established by the Department may be used.

LINE 26 Add Lines 21, 22, 23, 24 and then subtract Line 25 and enter the result.

LINE 27 Enter the total amount paid with this return.

Complete and detailed records of all sales, as well as income from all sources and expenditures for all purposes, must be kept so your return can be verified by a Department auditor.

YOU MUST COMPLETE THE SIGNATURE PORTION BY TYPING IN THE NAME OF THE PERSON SIGNING THE RETURN AND MAIL TO: Nevada Department of Taxation, PO Box 52609, Phoenix, AZ

local office.

DO NOT SUBMIT A PHOTOCOPY OF A PRIOR PERIOD FORM, YOUR FILING WILL POST INCORRECTLY.

If you have questions concerning this return, please call our Department's Call Center at (866)

SALES/USE TAX RETURN INSTRUCTIONS

Revised 01/04/2016

| Fact | Detail |

|---|---|

| Form Purpose | For use by sellers of tangible personal property registered with the Department of Taxation. |

| Notification Requirement | Sellers not selling anymore must notify the Department of Taxation. |

| Filing Requirement | A return must be filed even if there is no sales and/or use tax liability. |

| Address Changes | Business name or address changes must be reported to the Call Center at (866) 962-3707. |

| Penalty and Interest | Applies if postmarked after due date; based on NAC 360.395 for penalties and a set percentage for interest. |

| Mail Original | Mail original return to Nevada Department of Taxation, PO Box 52609, Phoenix, AZ 85072-2609. |

| Payment Details | Check payable to Nevada Department of Taxation; include tax ID number with payment. |

| Electronic Submission | Email form to nevadaolt@tax.state.nv.us with 'Sales and Use Tax Return' as the subject; attachments cannot exceed 10 MB. |

| Governing Laws | NRS 372.370 for collection allowance, and NAC 360.395 for late penalties. |

Filling out the State of Nevada Combined Sales and Use Tax Return demands meticulous attention to detail, ensuring that every data entry accurately reflects your business's sales and use tax liabilities. By accurately following the steps outlined, sellers of tangible personal property can ensure compliance with state tax regulations. This process not only helps in maintaining good standing with the Nevada Department of Taxation but also streamlines the financial operations of your business. Here's a step-by-step guide to correctly fill out this form, designed to make this mandatory task a bit easier to navigate.

Accurate completion and timely submission of the Nevada Combined Sales and Use Tax Return are crucial to avoid penalties and interest. By carefully following these steps and ensuring that all information provided is accurate, you'll maintain compliance and contribute to the smooth operation of your business within Nevada.

Who needs to file the Nevada Combined Sales and Use Tax Return?

Any seller of tangible personal property registered with the Department of Taxation in Nevada must file the Nevada Combined Sales and Use Tax Return. This includes businesses that conduct sales in Nevada, whether they are selling goods directly, supplying, or perhaps even performing transactions that are deemed taxable under state laws. It's important to file the return even if no sales or use tax liability exists for the reporting period.

What is the deadline for filing the return?

The return must be filed by the due date shown on the face of the return document. It should be postmarked on or before this due date to avoid penalties and interest. Timeliness is essential, as late submissions will incur additional costs calculated based on how late the return and payments are submitted.

How can I calculate the taxes due?

Total Sales (Column A) need to be reported at county level and include all sales related to your Nevada business excluding the sales tax collected.

Exempt Sales (Column B) are those not subject to tax, for various reasons such as sales to government entities or for resale.

Taxable Sales (Column C) are determined by subtracting Exempt Sales (Column B) from Total Sales (Column A).

Calculated Tax (Column E for sales tax and Column H for use tax) is figured by multiplying Taxable Sales (Column C or F) by the tax rate provided in the form, depending on the type of tax.

Moreover, a collection allowance is offered for timely filings, applicable only to sales tax.

What should I do if my business details change?

If there are changes to your business name or address, it is critical to contact the Department of Taxation Call Center at (866) 962-3707 immediately. Updating your account ensures you receive all necessary information and correspondence regarding your tax obligations and avoids complications with your tax returns and payments.

How do penalties and interest work for this return?

If your return or payment is submitted past the due date, penalties are calculated based on the number of days late, ranging from 2% to 10% of the net tax owed. The exact percentage increases with the number of days the payment is late. Interest is calculated at a rate of 0.75% per month for each month the payment is late. The system automatically calculates penalty and interest if the form is completed electronically and submitted late.

Filling out the State of Nevada Tax form requires attention to detail. Mistakes can result in penalties, interest charges, or incorrect processing of the form. Below are common mistakes that people make while filling out this form:

Being aware of these pitfalls can help in correctly filling out the State of Nevada Tax form, ensuring compliance, and avoiding unnecessary penalties or delays.

When filing the State of Nevada Sales and Use Tax Return, businesses engage with various documents essential for accurate reporting and compliance. These documents, often used in conjunction, can streamline the process, ensuring that taxpayers meet their obligations effectively.

Together, these documents play a pivotal role in the tax filing process for businesses in Nevada. They ensure that a business remains transparent, accountable, and compliant with state taxation requirements, safeguarding against discrepancies and potential legal issues. Managing these documents efficiently can significantly ease the burden of tax season, allowing businesses to focus more on growth and less on administrative challenges.